an phantasm… and 4 different issues we realized from Common’s newest earnings name")

{kind=link}

The information about Common Music Group following its newest earnings report yesterday (July 24) has been dramatic, to say the least: A double-digit inventory worth drop. A run of analyst downgrades. Hypothesis that the music streaming growth could also be hitting the skids.

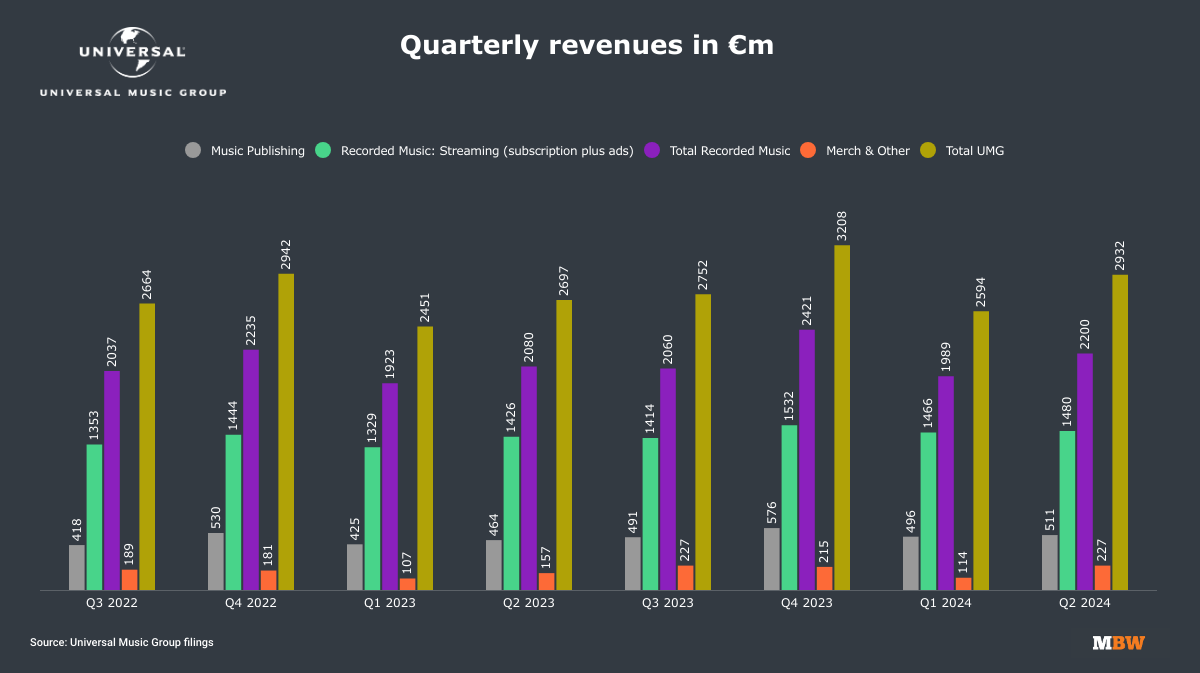

All of this was primarily based on a single metric: UMG’s streaming revenues in Q2.

To be clear, streaming revenues are nonetheless very a lot rising at Common. Most notably, subscription streaming revenues had been up 6.9% YoY in Q2 – but that fell wanting analysts’ estimates, which was for round 11% development.

The image was worse for ad-supported streaming income, which truly fell 3.9% YoY within the quarter.

Different measures of economic success, nonetheless, remained totally spectacular at UMG in Q2:

- Total revenues leaped up 9.6%YoY (at fixed foreign money), beating analyst expectations;

- Adjusted EBITDA grew 11.3% YoY, as much as EUR €649 million (USD $699m). This was additionally forward of analyst projections, in line with Seen Alpha consensus;

- Internet revenue soared 46% YoY within the first half of 2024, to EUR €914 million (USD $991 million), or €0.50 per share, in comparison with €0.34 within the first half of 2023.

The markets had been spooked nonetheless. UMG’s inventory worth fell simply over 23% at the moment (July 25) on the Amsterdam Euronext.

UMG additionally noticed a string of analyst downgrades, most of them from “purchase” to “maintain,” together with from Citi, Barclays, and Guggenheim.

It’s not a stretch to say that UMG’s management crew appeared to have seen this coming.

On Wednesday’s earnings name, unruffled UMG executives implicitly acknowledged that the streaming income miss can be on traders’ minds, providing quite a lot of feedback and explanations.

Maybe an important of these feedback: UMG isn’t notably apprehensive about this one quarter of slower-than-expected streaming income development; it’s enjoying an extended recreation.

“Internally, we don’t handle the enterprise on a quarterly foundation and are, subsequently, not overly involved once we see variation in our quarterly outcomes,” CFO and President of Operations Boyd Muir advised analysts on the decision.

“We now have a diversified enterprise mannequin, which accommodates quarterly variations, whereas nonetheless delivering stable development on the group stage.”

One other level UMG’s execs harassed: the occasional phantasm of efficiency weak point brought on by worth hikes at streaming companies over the previous few years.

Of specific notice this time round: Muir defined that worth hikes at Apple Music and Amazon Music that occurred greater than a 12 months in the past have now been “totally annualized” into UMG’s numbers, that means they not enhance Common’s YoY development.

(The identical factor will occur within the coming quarters with probably the most vital 2023 worth hike of all – the one at Spotify, which was executed in Q3 of final 12 months. For that reason, Guggenheim Companions analyst Michael Morris expects no pick-up in subscriber income at UMG in Q3 2024, coming in on the identical 6.9% charge as within the newest earnings report. He sees an additional softening of YoY development, to 5.3%, in This autumn.)

“Our second quarter outcomes replicate the numerous performances of our numerous portfolio of DSP companions.”

Sir Lucian Grainge, Common Music Group

In fact, not all the shrinkage in UMG’s streaming income development in Q2 was an phantasm.

A few of it was very actual, and UMG pointed to disappointing subscriber uptake amongst sure digital service suppliers (DSPs) – although the management crew didn’t identify names.

“Our second quarter outcomes replicate the numerous performances of our numerous portfolio of DSP companions,” UMG Chairman and CEO Sir Lucian Grainge stated, selecting his phrases rigorously.

CFO Muir elaborated: “Whereas Spotify, YouTube and plenty of regional and native platforms have continued to exhibit wholesome development in subscribers, different giant companions who’ve been much less profitable in driving world adoption have seen a slowdown in new subscriber additions.”

(You’ll discover, there, that Spotify and YouTube are off the hook; UMG is pinning the blame on softer subscriber development at sure different “giant companions” within the digital area.)

Muir added that UMG is “engaged with all our key companions in an in-depth dialogue relating to product innovation to focus on high-value clients and drive future income development.”

Total, Grainge harassed that UMG’s technique isn’t to chase after quarterly numbers, however to construct a robust enterprise in the long term.

“All through this journey of long-term development, we all know that quarterly fluctuations in a single income or one other are to be anticipated,” he advised analysts in his opening feedback.

“So whereas we report outcomes quarterly, we handle the enterprise for long-term success. We predict in multiyear cycles and anticipate and embrace variations in sure enterprise traces.”

Listed here are 4 different issues we realized on UMG’s earnings name – together with concerning the potential for Spotify’s new “super-premium” subscription tier, and a tantalizing trace that UMG’s catalog might quickly be accessible in different languages…

1) Had it not been for Meta and TikTok, ad-supported income would have grown

That wince-inducing 3.9% YoY decline in UMG’s ad-supported streaming income in Q2 would even have been a optimistic quantity (i.e., above zero), had it not been for 2 of UMG’s companions: TikTok and Meta Platforms.

Execs on the earnings name famous that UMG missed a month’s value of income from TikTok, when the music large had a high-profile falling-out with the video platform over its payouts, and UMG’s recorded and publishing catalog disappeared from the platform.

On high of that, there was additionally the truth that Meta Platforms pulled premium music movies off of Fb earlier this 12 months.

“Meta had beforehand supplied premium music movies on Fb. This product providing was much less standard with Fb’s consumer base than different music merchandise.”

Boyd Muir, Common Music Group

“By way of platform-specific stress, we’ve got a change in our licensing settlement with Meta,” Muir defined.

“Meta had beforehand supplied premium music movies on Fb. This product providing was much less standard with Fb’s consumer base than different music merchandise. And consequently, Meta is not licensing premium music movies from us as of Could this 12 months.”

Muir added: “Meta is now focusing as a substitute on different areas involving music content material, and we’re working collectively to develop these areas as a part of a multifaceted renewal.”

2) 20% of paying Spotify subscribers may join the brand new ‘super-premium’ tier

On Spotify’s earnings name earlier this week, co-founder and CEO Daniel Ek all however introduced that the long-rumored “super-premium” subscription tier is coming to the streaming service.

“The plan right here is to supply a a lot better model of Spotify,” Ek stated.

“One thing like $5 above the present Premium tier… kind of a deluxe model of Spotify that has all the advantages that the traditional Spotify model has, however much more management, lots increased high quality throughout the board, and another issues that I’m not prepared to speak about simply but.”

Although Ek was reluctant to get into particulars, he floated a attainable $17 or $18 per 30 days worth level.

It’s extensively anticipated that the super-premium tier will (lastly) give Spotify listeners entry to high-fidelity audio, and it could additionally embrace options equivalent to “superfan golf equipment.”

We even have some market analysis on the plan’s potential, courtesy of UMG.

“Our analysis and evaluation point out that as many as 20% of the present subscriber base may improve to a super-premium tier at a meaningfully increased worth level for a compelling product configuration, one which presents enhanced options and unique entry to content material,” Muir advised analysts.

Provided that Spotify reported 246 million paying subscribers in Q2 2024, UMG’s estimate implies that some 49.2 million of them would join super-premium.

And if that plan does, certainly, price $5 extra per 30 days than the usual Premium tier, that interprets to $2.952 billion in further annual income for Spotify. (Assuming that the super-premium tier will price $5 greater than Premium in all markets, which isn’t essentially a protected guess.)

And assuming that Spotify pays out two-thirds of its income to music rights holders, that quantity would characterize further revenues of $1.966 billion to the music trade.

So the tip of the streaming growth might not but be at hand…

3) UMG sees 180 million potential new streaming sign-ups in high markets

Apart from the potential of “super-premium tiers,” UMG is of the opinion that there’s nonetheless loads of room for extra sign-ups to music streaming companies, together with in mature, developed markets.

In UMG’s market analysis, “we’ve recognized an addressable market of over 180 million shoppers that can kind the subsequent wave of subscription adoption” throughout the high 19 music markets, UMG Chief Digital Officer Michael Nash stated on the decision.

“And that analysis is performed assuming worth will increase. About half of that whole addressable market might be within the 13 developed markets.”

He stated that UMG expects to see “a number of development” in rising markets.

“It’s vital to take into account that know-how innovation, digital infrastructure penetration, rising shopper traits, all this stuff have been persistently rising the overall addressable marketplace for subscriptions during the last decade,” he added.

Certainly, whole paid music streaming accounts hit 503 million worldwide on the finish of 2023, up 13.2% YoY, in line with information from IFPI shared by label sources. There have been 667 million customers of subscription streaming accounts in 2023, greater than double the quantity in 2019, however nonetheless solely round 8% of the world’s inhabitants.

4) Basic songs in UMG’s catalog may quickly be showing in different languages

Not all of UMG’s earnings name was about streaming subscription development – a few of it centered on the opposite obsession within the music trade nowadays, specifically AI.

UMG just lately introduced a partnership with SoundLabs, an AI know-how firm centered on “ethically educated” instruments for music creators.

One key product from SoundLabs is MicDrop, a vocal plug-in that allows artists to create high-fidelity vocal fashions utilizing their very own voice information.

One upshot of that, in line with UMG’s Grainge, is that we may quickly be listening to traditional songs from UMG’s catalog – sung in varied languages aside from those they had been recorded in.

UMG’s artists “will have the ability to sing in languages they don’t converse, restore imperfect vocal recordings, and extra,” Grainge stated on the decision.

“The power to have the ability to sing in their very own voices in languages they don’t converse opens up huge potential and massive alternative for us to promote, market, transfer tradition and create demand for songs and merchandise and again catalog that may have been fully unimaginable,” he added, calling the prospect “very thrilling.”

On this entrance, UMG can profit from the “proof of idea” carried out by different music corporations.

Final 12 months, South Korea’s HYBE launched a Okay-pop monitor – Masquerade by MIDNATT – in six totally different languages, due to know-how developed by Supertone, an AI voice-cloning firm that the Okay-pop large acquired in 2022.

A number of months later, Tencent Music-owned streaming service Kugou Music unveiled KUGOU AIK, which alters singing vocals into 10 languages and 15 Chinese language dialects.Music Enterprise Worldwide